Home Mortgage Guidance You Need To Hear

Authored by- https://www.moneysavingexpert.com/news/2021/09/banking-hiya/Are you looking for information on home mortgage information? There is a lot to know when it comes to home loans. Regardless of what brought you here, it is possible for everyone to get some useful home loan information from this article.

Have at least 20 percent of the purchase price saved. Lenders will want to verify that you have not borrowed the money, so it is important that you save the money and show deposits into your checking or savings account. Down payments cannot be borrowed; thus it is important to show a paper trail of deposits.

Get your documents ready before you go to a mortgage lender. You should have an idea of the documents they will require, and if you don't, you can ask ahead of time. Most mortgage lenders will want the same documents, so keep them together in a file folder or a neat stack.

Predefine your terms before applying for a mortgage, not just to show the lender that you can handle the arrangements, but to keep your monthly budget aligned as well. Buy a house that fits into your budget. No matter how much you love the home, if it makes you unable to keep up with your bills, you will wind up in trouble.

Start saving all of your paperwork that may be required by the lender. These documents include pay stubs, bank statements, W-2 forms and your income tax returns. Keep these documents together and ready to send at all times. If you don't have your paperwork in order, your mortgage may be delayed.

If you are offered a loan with a low rate, lock in the rate. Your loan may take 30 to 60 days to approve. If you lock in the rate, that will guarantee that the rate you end up with is at least that low. Then you would not end up with a higher rate at the end.

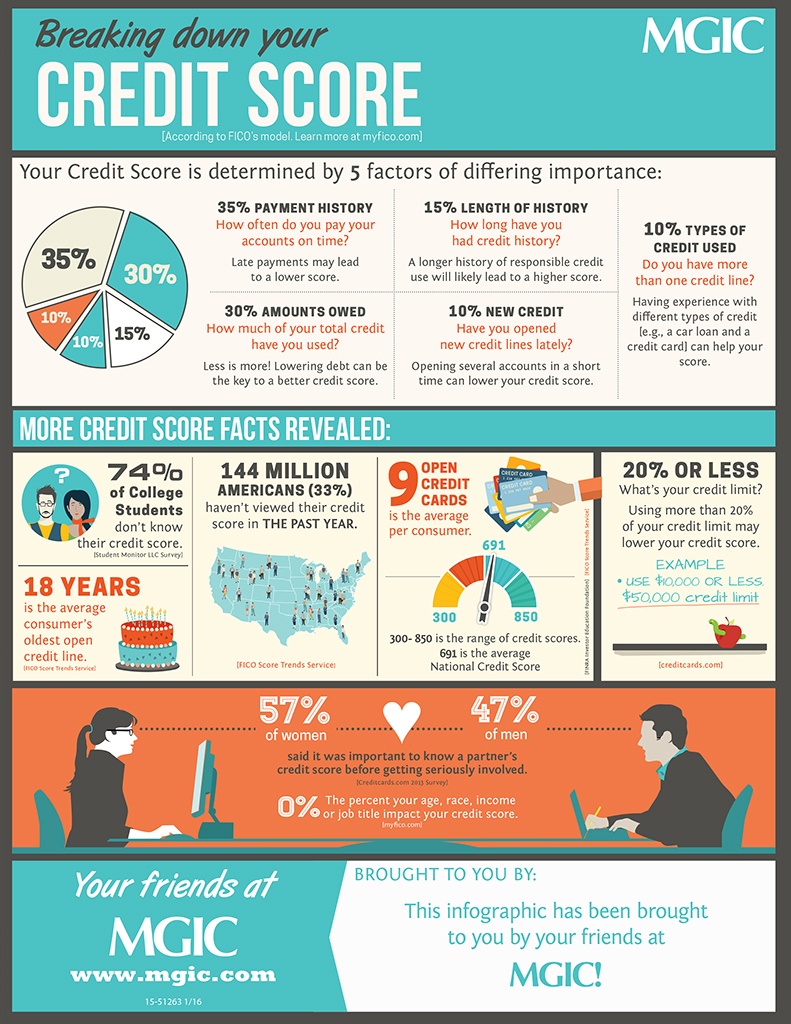

Make sure that all of your loans and other payments are up to date before you apply for a mortgage. Every delinquency you have is going to impact your credit score, so it is best to pay things off and have a solid payment history before you contact any lenders.

Save your money. When you are going to finance a home mortgage, you will need to have some cash for a down payment. The more money you pay down, the lower your payments and interest rates. The down payment goes directly to the principal of the mortgage and is a sum you will not owe yearly interest on.

Refinancing a home mortgage when interest rates are low can save you thousands of dollars on your mortgage. You may even be able to shorten the term of your loan from 30 years to 15 years and still have a monthly payment that is affordable. You can then pay your home off sooner.

If you have filed for bankruptcy, you may have to wait two or three years before you qualify for a mortgage loan. However, you may end up paying higher interest rates. The best way to save money when buying a home after a bankruptcy is to have a large down payment.

Before you even start looking at a new home to buy, try to get pre-approved for a home. This will give you confidence when looking for a new home and let you know what your budget is. It will also save you from choosing a home only to find out you cannot secure a large enough loan to purchase it.

Pay off or lower the amount owed on your credit cards before applying for a home mortgage. Although your credit card balances do not have to be zero, you should have no more than 50 percent of the available credit charged on each credit card. This shows lenders that you are a wise credit user.

If you are a retired person in the process of getting a mortgage, get a 30 year fixed loan if possible. Even though your home may never be paid off in your lifetime, your payments will be lower. Since you will be living on a fixed income, it is important that your payments stay as low as possible and do not change.

Make sure that you compare mortgage rates from several companies before you settle on one. Even if the difference seems to be minimal, this can add up over the years. One point higher can mean thousands of extra you will have to shell out over the course of the loan.

Remain honest through the whole loan process. If you aren't truthful, you may be denied the loan you seek. If check out the post right here can't trust you to tell them the truth, then they likely won't want to lend you money.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. This could open a new avenue of financing up for your new home mortgage.

Take note of home buying season. Usually markets will have hot and cold selling periods. The hotter the selling period, the more shady lenders are likely to be around. If you know what trend the market is in, you will better be able to guard against people looking to take advantage of you.

After your mortgage is approved, continue to manage your credit responsibly. Your mortgage broker will check your credit again before finalizing the deal. If you decide to go out and charge a trip to Tahiti on your credit card to celebrate your new home, you could very well lose your home mortgage! Simply sit tight and continue making timely payments on the debts you have until you are firmly situated in your new home.

When the bank asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

Many people get denied when applying for a home mortgage because they don't understand what they need to do in order to get approved. If you have been denied in the past or this is your first time applying for a home mortgage, then use the tips here to better prepare yourself for the process. Be smart, read over these tips and you will get approved for a home mortgage.